Original story from Dagens Nyheter (in Swedish)

If the pension statement gives you the creeps, and you can only manage one thing in the orange envelope, then you should focus on the forecast on page five in your Swedish pension statement, says Arne Paulsson at the Pension Agency.

The prognosis in your Swedish pension statement is very uncertain if you are 30 years old or younger but it can give you an idea of how much you will receive in retirement. The closer to retirement you are, the more accurate the forecast is and this is the time to really think about when to retire, says Arne Paulsson.

He also points out that none of the information in the envelope actually affects your pension. However, what does affect it are things like deciding to work full time instead of part time, paying taxes on your salary or working beyond the age of 65. So basically – stop worrying, open the orange envelope and increase your knowledge.

So how do you actually read your Swedish pension information?

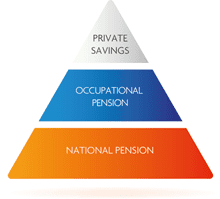

Page 1: The pension triangle

The first page displays the pension triangle. The base represent the Public pension you receive from the state. Below the triangle, three boxes show how much you earned for your retirement this year, your total savings and how much money you are expected to receive when you retire.

Page 2: Swedish pensionsrätter

The second page of your Swedish pension statement is about something called “pensionsrätter”. Which basically means the money that employers and individuals pay into you pension during the year. One part is “inkomstpension” which you do not manage yourself, and the other part is called “premiepension” wich you are free to manage yourself. Make sure that you check on what forms the basis of your “pensionsrätten”. You should note that in addition to your normal income, you have the right to pension earnings from parental, unemployment and sickness benefits.

Page 3: Changes in Swedish pension value

The third page shows how the value of your Swedish pension has evolved during the year. You cannot affect the change in value of the “inkomstpension” which varies each year. This year it had an increase of 5.8 percent. The statement showa the increase in value for the premium pension next to it. There you also get information about how much you’ve paid in fees.

Here you also get information about inheritance profits. The system allocates these pensions each year to surviving pension savers. This is nothing you can influence either.

Page 4: The premium pension

The fourth page focuses on the premium pension, (PPM), an important part of the Swedish pension system. This is the small part you can influence yourself by selecting funds and stocks. Here you see where your PPM money is invested and how much you pay in fees. Of course, you also see the value increase in percent. Are you dissatisfied with the results? Change funds. Those who do not make a choice will have this section of their pensions placed with Sjunde AP–fondens Såfa which has a low fee and usually steady development.

Page 5: Your retirement forecast

The last page is your future prognosis based on the age you choose to retire. This part of the prognosis usually interests people as it is easy to see how much more you get if you work a few extra years within the Swedish pension system.

For more information, visit the Pension Agency and choose the language of your choice.